What am I teaching next?

In Summer 2026 (June): corporate taxation (English)

In Fall 2026: introductory tax course

(FR & EN, two sections)

Office hours: TBD

Use Word's Style formatting tools to organize your document so you can analyze its structure and flow for better academic writing.

really basic rules for diagramming commercial, corporate and tax law scenarios

Introduction to Tax Policy theory:

How to write a case comment

A case comment is designed to introduce a reader to a case and situate it within its topical, analytical, historical and social context. The point of the case comment is not simply to summarize or exhaustively re-state the case. Instead it is to focus the reader on a particular aspect of the case that is significant or interesting in some way. Your description of the case should begin with a few impactful sentences that lay out the controversy (why are the parties in court), the respective parties’ core positions, and the outcome of the case (taxpayer wins or government wins). A good case comment will have considered the factors that led the parties to take the controversy to the courts and it should help the reader who may not have read the case get the main ideas that emerge in the decision.

Include the name of the case, its proper citation, and a link, preferably to CanLII, as well links to lower court decisions and that judge’s or those judges’ names, if you are presenting an appellate decision (TCC or FC decision and FCA decision, if any).

A good case comment begins from the start of the reading process. When reading tax decisions, the particular takeaway may not be the ratio decidendi of the case. It is perhaps more important to see how the judge(s) reasoned with the lower court decisions or the statutory framework (i.e., their construction of the Act’s words). Also, as a reminder that tax is a team sport, note that your reading of a particular passage or provision may be different than that of your teammate(s). Explore why you and your teammate(s) arrive at different readings. Discussion brings cases to life and often exposes more thoroughly areas we thought we understood.

A good case comment tells a story about the case. It should be dynamic, use active voice, and avoid abstraction and cliché. It should be short, well written, punchy, to the point, non-repetitive, and informative. When you write a case comment it can be helpful to think of yourself as a journalist and ask yourself the questions that order a news story: who, what, when, where, and why. Who is in court? Why are they in court? What problem are they trying to solve? What approaches and sources did they use to persuade the judge(s) to see things their way? How did the judge(s) approach the problem? What issues were resolved, and what issues were not resolved? Provide answers to these questions.

A great case comment will locate information about the parties, their transactions, or the evolution of the applicable law that isn’t included in the case, but that lends clarity to the narrative of the case or the particular “mischief” at play. Most of all, a great case comment provides an original and critical take on the particular issues of the case.

How to write a tax law memo or legal opinion

If you write any kind of document that provides legal analysis, opinion, or advice (hereinafter, collectively or individually, a “memo”) that will be given to a client, the following advice might be helpful to you.

1. Indicate the audience and the topic with standard memo lines at the top of the page, like so:

Date: [not strictly necessary but customarily expected]

To: [the imagined audience of your memo]

From: [can be a pseudonym or title as a placeholder]

Re: [the legal issue in a few words. Be pithy.

2. Start the discussion by stating the question to be answered, in one sentence.

(a) When the audience is a taxpayer (aka client), this means: what is the client’s issue? In federal income tax law, the issue always turns on some provision of the Income Tax Act (“the Act”). Every client question emanates from a specific statutory rule that ultimately requires the client to pay a specific amount of tax at a specific time. Every client question that involves federal income tax law is therefore about figuring out (a) who the taxpayer is, (b) what is going to be taxed, and (c) when; all for federal income tax purposes (you must accordingly indicate the scope of your analysis and not accidentally stray into provincial or territorial tax analysis or (worse) start talking about things that have nothing to do with the tax law, such as tort liability).

When a taxpayer comes to you for advice, they do so because:

They are going to take a course of action depending on the expected tax consequences of taking such action, often in light of one or more alternative courses of action; or

They are going to take a position on a tax return about a given item of income or deduction or loss; or

They already took a course of action and a position on a tax return and are facing opposition against their expectations from the CRA; or

They already took a position, faced opposition from the CRA with which they disagree, and are preparing to take the issue to a Court to decide the matter. Often, students err in thinking that all questions are questions about how a court or a judge will view a matter. Most are not.

When giving your tax advice you must accordingly state the problem to be solved or the question to be answered in terms relevant to the specific situation.

(b) Even when the immediate audience of your writing is a person senior to you in a law firm or in-house legal team, your audience is ultimately the client/taxpayer. Your senior person wants the memo you are writing to support a legal opinion they will give to the client. Therefore, all of the above applies.

(c) When the audience is a person senior to you in the CRA or the DOJ, this means: what is the CRA’s or the Government’s (or Appellant’s/Respondent’s, where appropriate) view of the tax consequences of a given taxpayer’s action? The memo should proceed in the exact same manner as it does for a client, that is, starting with a question that emanates from relevant provisions of the Act. Your job in writing a memo to this audience will be to state the position of the CRA or the DOJ (“Our position is”) and defend the correctness of the position taken. You must therefore understand and address the taxpayer’s question as they frame it, but you are not confined to the taxpayer’s framing. Note also that when you are writing as an agent of the CRA, if you argue a point using CRA guidance, you are effectively arguing your own position to yourself. It does not make sense to do so in the third person (“The CRA states that…”). Moreover, note that your own position on a matter is not inherently dispositive; rather, it is a position with which the taxpayer is likely to disagree. As such, it is not enough to simply restate your position as if this ends the argument. The taxpayer’s argument against you will be that your position is incorrect, or at least incorrectly applied to them, and you must reason through the argument accordingly.

(d) When the audience is a judgefor whom you are clerking, this means: what is the correct legal interpretation of the relevant law? The parties’ opposing positions are supposed to help you understand the range of possible interpretations, but you are undertaking to assist the judge in their legal decision-making so you are not confined to the arguments of either party as to the scope of the issue to be decided.

3. Answer the question by taking a positionto be defended, in one sentence.

This means you must decide what the answer to the question is and state it in terms that properly convey your sense about the possibility that your answer is wrong.

(a) When the audience is (a) or (b) above, this means: state your legal opinion in a way that indicates your level of “comfort” with your answer. Comfort levels are the culture and the currency of tax practice, and there is no single rule, standard, or norm to follow. A person’s level of comfort is something that is gleaned through experience and personal conviction, all of which is passed on to associates and colleagues through collaboration. That said, experts share familiar, if imprecise, expressions of comfort in tax opinions such as “more likely than not” and “the better view,” and you will learn these terms should you ever find yourself as a tax law practitioner in virtually any context (see the tax opinions chart below).

Note that a “will” (or “will not”) opinion is a strong opinion. It says that you are confident that your analysis is 100% correct and there is no room for ambiguity. A “may” opinion is the opposite. It is a weak and noncommittal response that tells clients that you are not willing to take a stand.

Lawyers do not typically give and clients do not typically like to pay much for “will” opinions because if an issue of law is perfectly clear, the client typically has little need for the expensive assurance of a legal opinion. Lawyers don’t mind telling clients if something “will not work” in contravention to advice they might have received elsewhere. Lawyers might like to give, but clients do not typically wish to pay for, “may” opinions because they do not give the client much confidence or direction in how to proceed.

(b) When the audience is (c) or (d) above, this means: state your position in a way that indicates the degree of uncertainty surrounding it. In the CRA or DOJ scenario, the idea is that you are indicating the best position in your view but alerting to the risk of opposition by the taxpayer and, in the case of the DOJ, by a judge. In the clerking scenario, judges will often want to understand the strength of the position in order to precisely tailor the scope of their decision. Whether you are expected to take a specific position and defend it may depend on the particular judge for whom you are clerking. Some may wish you to take a position and defend it while others may wish you to argue both sides vigorously without taking a stand. If you are unsure: take a position and defend it.

4. Set out the organization of the defense of the position to follow in the rest of the memo.

This “signposting” or “road-mapping” will guide the reader but a main reason to do this systematically, in essentially everything you write in law school, is to organize your research and make your writing coherent. In a tax law memo, it is common to present a roadmap in the form of a bullet point (brief) recitation of the reasons justifying the conclusion you stated in answer to the question you posed. The subsequent discussion must follow the roadmap.

5. Restate the relevant facts and assumptions only to the extent necessary and useful.

(a) A (re)statement of facts is not always strictly necessary but a brief recitation can aid in jogging the memory of the reader who assigned you the research, whether the client or a senior person. Make it brief. Often you can state only a few key facts and say “other facts are as you stated them in your memorandum to me” or similar.

(b) Do not add facts to make your analysis easier. Especially: do not add facts and call them assumptions. Example: “I assume that the company provided the worker with a cell phone.” In a memo that seeks to determine whether the worker is an independent contractor for federal income tax purposes, the ownership and use of tools is a component of the underlying legal analysis. If adding facts tilts the balance of the analysis, you must not add them. If you cannot make a determination regarding a part of the analysis without more facts, that is something to state at the relevant part of the analysis. If you believe you do not have enough facts to formulate a position in response to the question at all, you must so state in your answer to the question. However, your senior colleagues will not typically send out such a memo and, where relevant, your client will not wish to pay much for such a memo. In virtually all cases you must come to a conclusion based on the facts as you have been given them, state with specificity in your analysis where and in what way missing facts would be determinative as to the outcome, and state how the outcome would differ depending on the missing facts.

(c) Do not include statements of law in your recitation of facts or assumptions. Statements of law are neither facts nor assumptions when they are the subject matter of the question being answered.

Example: In a memo determining whether someone is properly characterized as an independent contractor for federal income tax purposes, you may not state as an assumption that “The client is engaged in a business” because this is a conclusion of law that goes directly to the question asked.

When writing assumptions, ask yourself: why do I require this assumption? If the reason you give yourself is “to make it easier to take a position,” stop: this is not an assumption, it is an end run around the uncertainty inherent in answering questions about tax law.

6. Defend your answer, following the roadmap you set out above.

And here are some bonus pro tips:

Do not jump to case law without explaining why it is that we need to consult jurisprudence. As mentioned above you must state with clarity why you are inviting the reader to consider this source of law. The only way to do that is to show the path from the statute to the case.

You must always start with the relevant provisions of the Act, otherwise there is no problem to be solved. You should typically start with a charging provision and explain the path from the relatively straightforward charging provision to the interpretation and application problem to be solved.

Here is an example: ITA subsection 2(1) provides inter alia that an income tax shall be paid “on the taxable income for each taxation year of every person resident in Canada at any time in the year.” The term “resident in Canada” is not defined comprehensively in the Act. Subsection 250(1) deems certain individuals to be resident in Canada according to specified factors [if not relevant to the facts at hand, state why not]. Subsection 250(3) adds that “a reference to a person resident in Canada includes a person who was at the relevant time ordinarily resident in Canada.” The meaning of the term “ordinarily resident in Canada” is not given in the Act. Common law has interpreted this term to mean…. etc.

Make your life easier by stating at the outset “Unless otherwise noted, all statutory references herein are to the Income Tax Act, R.S.C., 1985, c. 1 (5th Supp.).” That way you can simply use the correct unit of federal legislation designation without having to add “of the ITA” or similar throughout.

Never say “one could argue” or “it is possible to argue”. Anyone can argue anything. The question is not what range of arguments exist in the world, but rather: what arguments are persuasive? Why, in terms of the applicable doctrine, are they persuasive? What are the likely counters to the argument and how persuasive are they?

Avoid making the opinion personal. The reader does not want to learn what “I think” or “I believe.” The reader wants to learn my informed legal opinion, and the strength thereof based on the facts and the relevant law.

Never cite a secondary source for a claim about the content of a statutory provision. It looks like you are either too lazy or too afraid to read the primary sources and cite them. In all cases you must start with the relevant statutory provision, and you consult case law when the statutory provision requires interpretation beyond the plain meaning. Only seek out a secondary source when all of the primary sources (statutory and case law) do not yield a clear result, and you are looking for persuasive arguments to support your own interpretation of a given provision.

Avoid using passive voice. Passive voice nearly always signals a drafter’s lack of comprehension regarding the purpose of the memo, the scope of the argument, the audience, or the logic of the arguments presented. Even if the drafter doesn't lack comprehension, using passive voice makes it hard for the reader to figure out what is going on, which produces doubt and lack of trust in you, the advice-giver. It is simply better in every case to avoid passive construction unless you’re intentionally trying to obfuscate, for example to hide your unwillingness to give a strong opinion.

Example: “If it is found that the taxpayer…” found by whom? Found in what sense? Do you even know?

If you are not sure whether you are using passive construction, look at your sentences and ask yourself, can you add “by zebras” anywhere and it would still make grammatical sense? If so, congratulations, you’re using passive voice. Now stop that. Example: “If it is found by zebras that the taxpayer…”

Indicate the strengths and weaknesses of each argument you make, and guide the reader as to how to interpret your preliminary or intermediary conclusions.

Don’t let facts speak for themselves. Even if the implications of an observation you make seems perfectly clear to you as the drafter, do not assume that the same will hold true for the reader. State your observation and then state the significance of the observation explicitly.

Conclude succinctly by summarizing the position and the key risks, and invite the reader to return to you if they wish to discuss further.

In student writing, the invitation to return to you is a courtesy but it is good to form this habit early.

And finally, a practice note: In all likelihood if your draft is well written, the senior person will use it as the template for the legal opinion they will give the client, and they will view you as someone who adds value. If it is poorly written, they will either see your potential and try to train you to do better or they will begin not to trust you with this type of work at all. Getting extensive feedback and comments may indicate the former so you must learn to welcome and appreciate feedback. Do not take negative feedback as a personal attack unless it is expressly an ad hominem attack. Any attack of the analysis itself is constructive even if it is given in harsh terms. Learn to hear the feedback instead of the tone of it. That said, when you are the person giving feedback, try to remember that a person with great potential could be lost to a competitor over the pain of repeated exposure to an overly harsh tone.

Tax opinion letter

As a client, you want to be able to go back to your lawyer and say “you told me to take this course of action or take this position and you were wrong, so you pay for the interest and penalties.” A lawyer does not want any risk as to such an eventuality. Hence writing comfort levels into tax opinions is an art form, and a high stakes one at that.

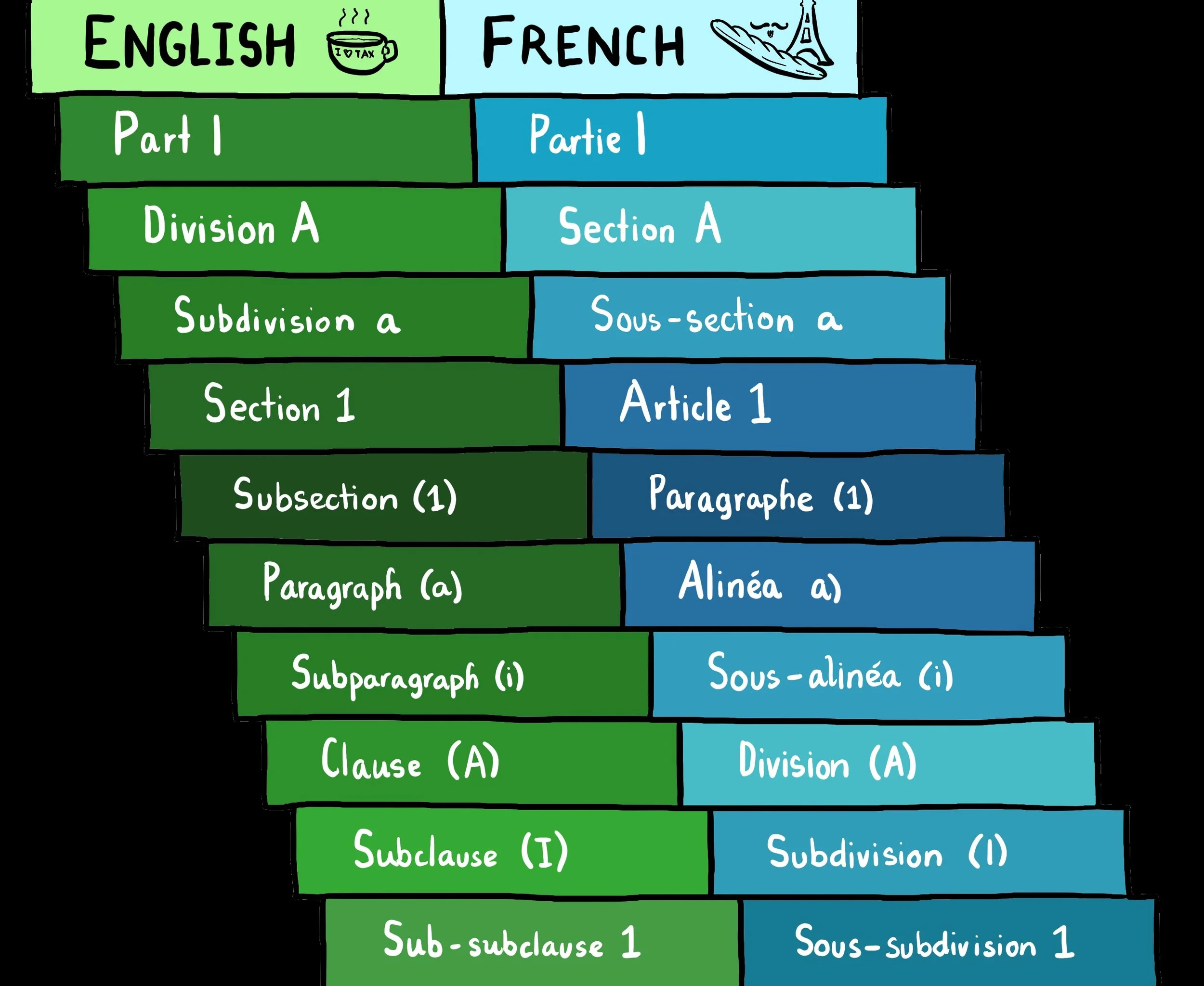

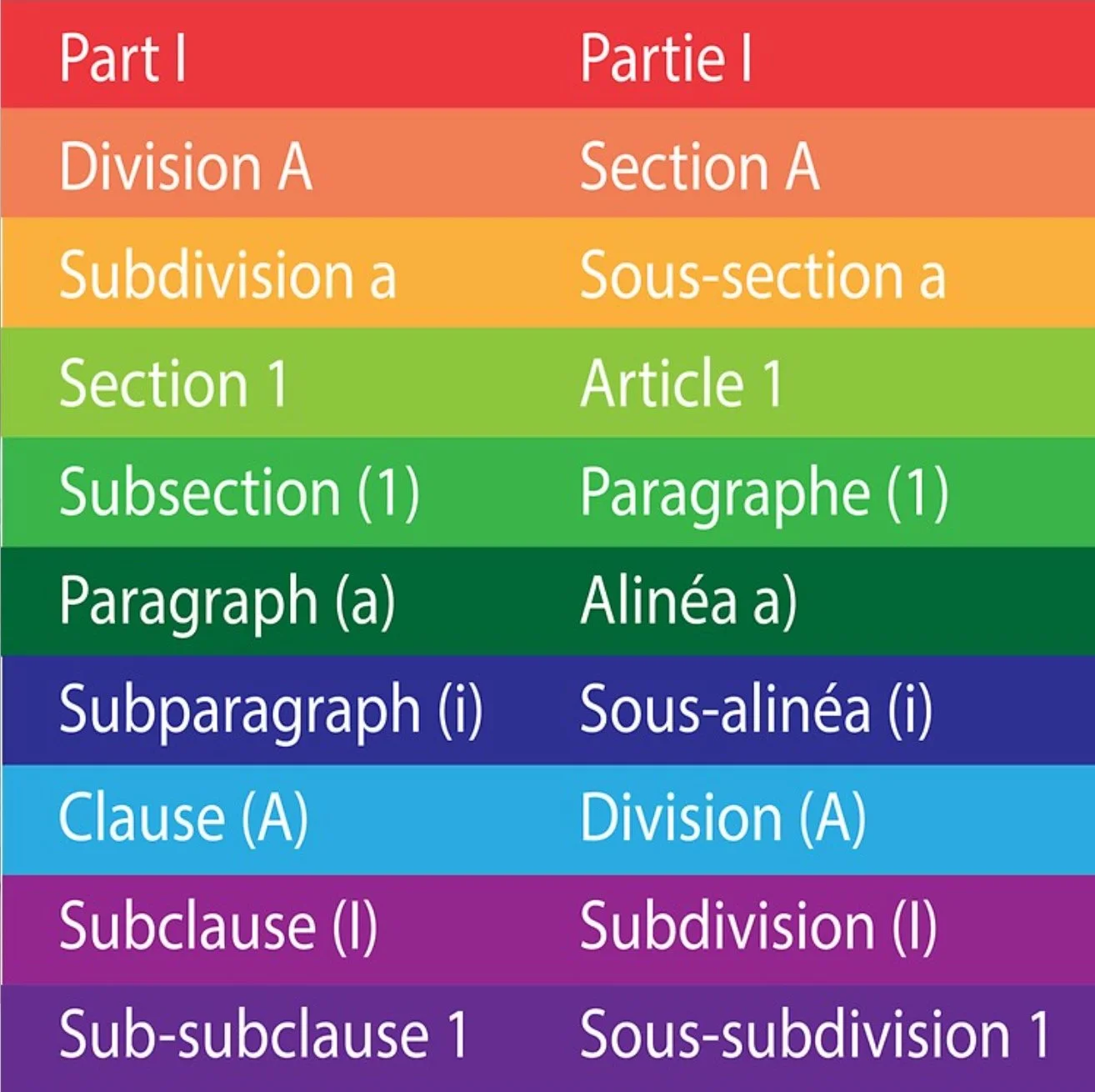

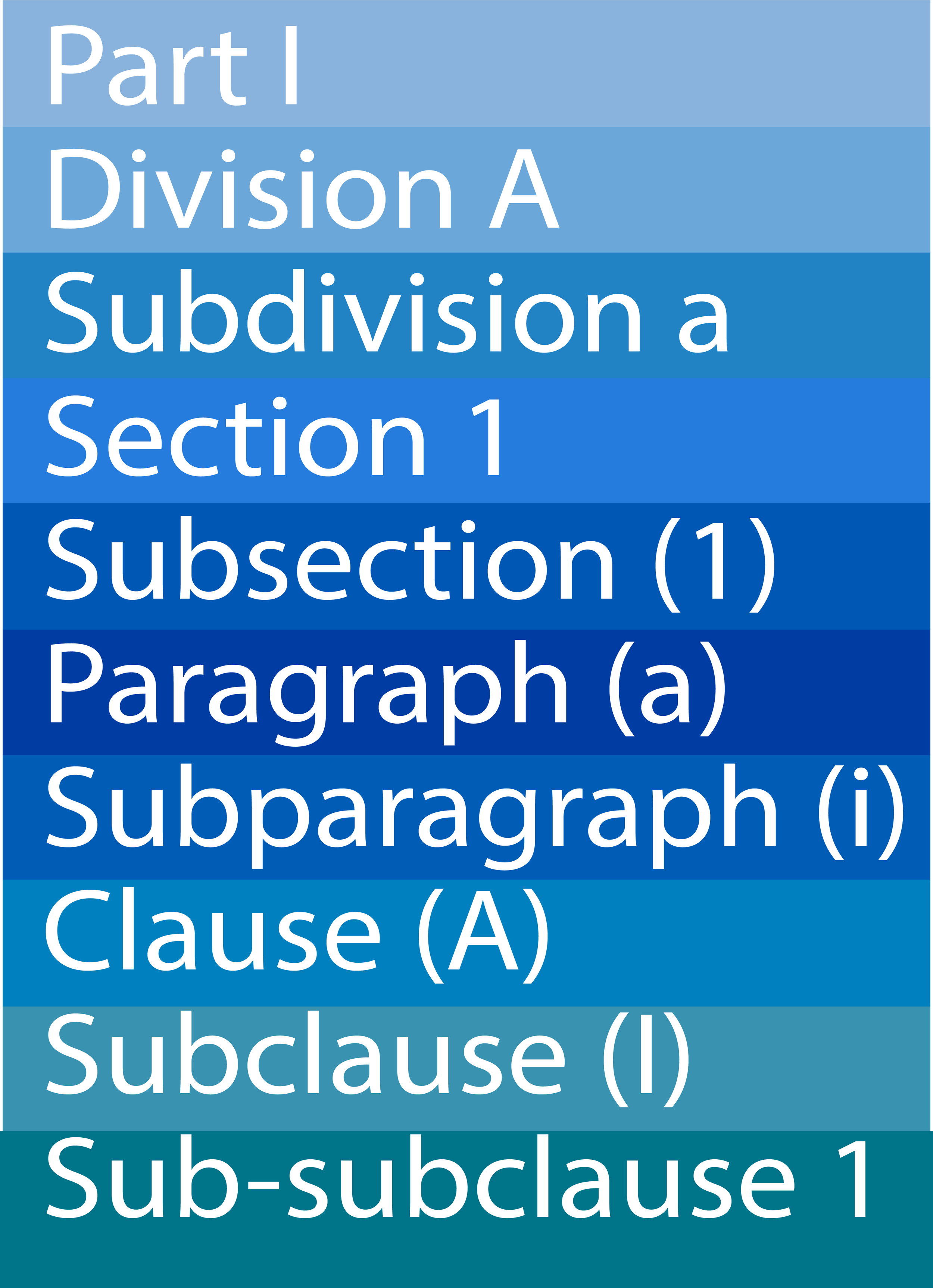

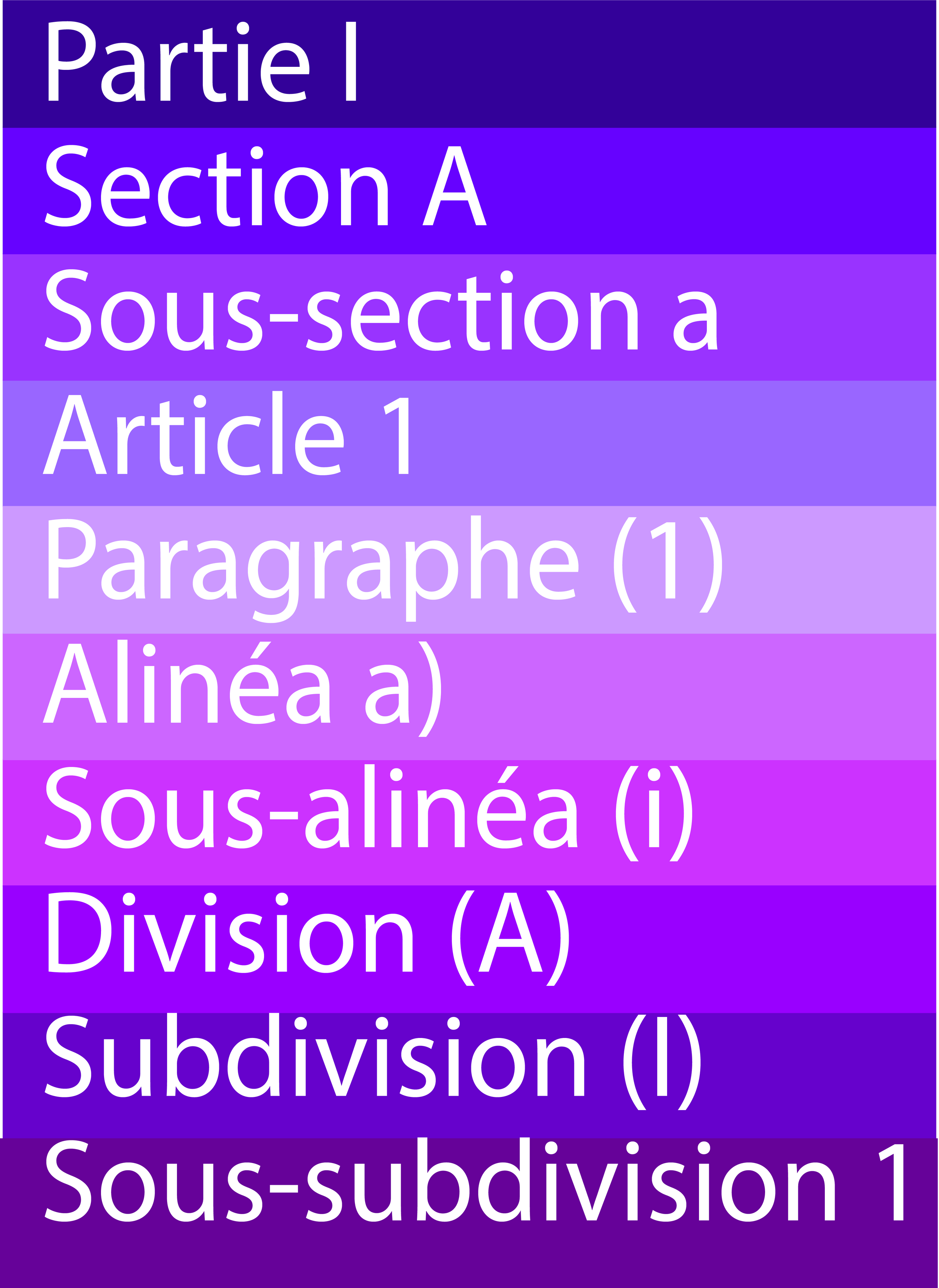

Units of federal legislation

This handy chart is essential to anyone writing a legal memo in Canada involving federal income tax law + any other federal statutory regime.

It tells you how to identify a specific part of legislation in Canada.

For example, if you are looking at a provision of a federal Act online that starts with a lower case roman numeral in parentheses, you will know that you are looking at something that is called a “subparagraph” in English and un “sous-alinéa” en Français.

When writing out a specific provision, it is customary to state only the unit associated with the last numeral according to its format. For example if you are looking at the rule that says to include in income the value of an employee benefit related to the use of an automobile, you would not refer to “subparagraph (iii) of paragraph (a) of subsection (1) of section 6” or “le sous-alinéa (iii) de l’alinéa a) du paragraphe (1) de l’article 6). That’s way too clunky. Instead, you would refer to the relevant provision as “subparagraph 6(1)(a)(iii)” aka “le sous-alinéa 6(1)a)(iii)”

Knowing the correct unit of legislation will help you figure out where to look when someone points you to a provision, and vice versa.

Do you need this chart on a sticker, mug, mousepad, poster, or something else? Find one here.